Providing a Bridge Over the OZ Funding Dead Zone

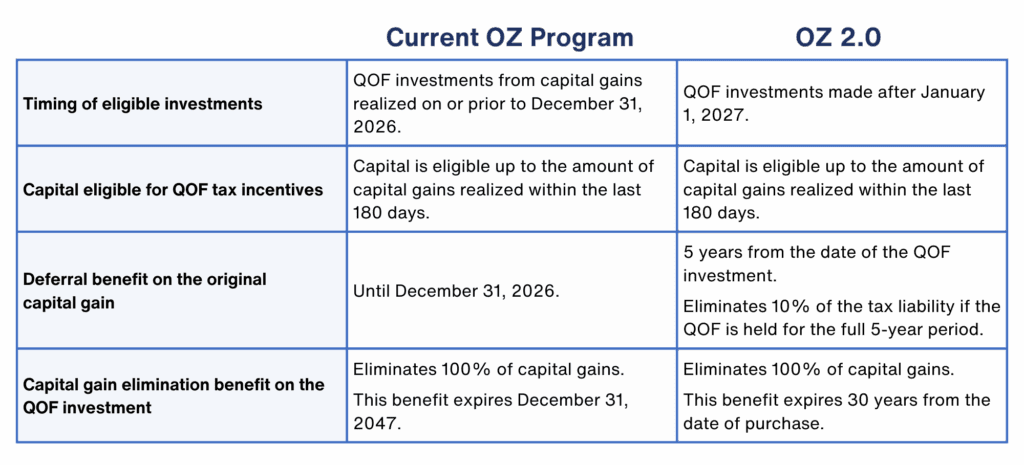

The new permanent Opportunity Zone (OZ) legislation offers enhanced tax incentives, but only for investments made into Qualified Opportunity Funds on or after January 1, 2027. The issue primarily affects investors whose 180-day Opportunity Zone investment window closes before the enhanced incentives become available on January 1, 2027.

Under QOF rules, capital gains need to be invested into a QOF within 180 days of the gain being realized. This means that gains taken before July of 2026 will, in most cases, not be eligible by the time the enhanced tax incentives roll out in 2027. Many observers fear that this will unintentionally create what the law firm Baker Tilly describes as a “Dead Zone” for investments in OZ communities [1]. We agree that it is highly likely that many investors will wait for the enhanced benefits to become available. This situation will frustrate taxpayers and result in capital investment slowing in the very communities the program was designed to support. This is clearly counter to the purpose and intent of the legislation.

The Bridge Strategy Solution

The existing regulatory framework may already provide investors with a pathway to bridge the gap between current Opportunity Zone incentives and the enhanced benefits scheduled to begin in 2027.

Under the final Opportunity Zone regulations, a previously deferred capital gain recognized from the disposition of a Qualified Opportunity Fund (QOF) investment can itself qualify as newly realized eligible capital gain. This creates a fresh 180-day window in which the proceeds may be reinvested in another QOF, allowing the deferral to continue [2].

Funds structured with sufficient holding-period flexibility may be able to support this type of “Bridge Strategy.” This approach may help ensure that capital continues to flow into Opportunity Zone communities rather than remaining on the sidelines during the transition period.

While this strategy involves inherent risks, it could help sustain investment flows to Opportunity Zone communities during the transition period, provide investors and tax planners with additional planning flexibility, and preserve the eligibility of capital to access the enhanced Opportunity Zone 2.0 incentives once they take effect in 2027.

According to the accounting and tax advisory firm, BDO, “Investors holding qualified investments in QOFs should consider the following approach(es) to mitigate exposure to income taxes related to a gain deferral recognition event: Completing a sale or exchange of a QOF investment or underlying QOZ property before the mandatory recognition date and re-deferring the gain into another QOF investment. The IRS regulations allow taxpayers who recognize eligible deferred gain resulting from an inclusion event to re-defer that gain into another QOF investment.” [4]

Under the Opportunity Zone rules, taxpayers generally have 180 days from the realization of an eligible capital gain to invest that gain in a Qualified Opportunity Fund (QOF). Investors who realize gains late enough in 2026 may have reinvestment windows that extend into 2027, allowing them to access the enhanced incentives once they take effect.

The problem arises for investors whose eligibility windows expire before the end of 2026. These investors may be reluctant to commit capital under the diminished incentive structure of the original program, yet they cannot wait for the enhanced OZ 2.0 incentives because their eligibility period will have already closed.

The Bridge Strategy is designed to address this specific group of investors. By deferring capital gains through a QOF investment today and later selling that QOF investment, a taxpayer may trigger a new capital gain realization event and a new 180-day reinvestment window, potentially allowing the gain to be reinvested and capture the enhanced incentives once they become available in 2027.

In this way, investors can keep their options open while continuing to participate in the Opportunity Zone program, helping maintain investment flows into Opportunity Zone communities during the transition period.

Implementing OZ Tax Planning Examples:

This mechanism has the potential to serve as a bridge between OZ 1.0 and 2.0, keeping investors from moving to the sidelines during an unintentional “Dead Zone” period. Here are a few examples illustrating how investors might evaluate their expanded OZ tax planning options.

How an investor with a recent capital gain might benefit from the Bridge Strategy.

- A taxpayer may recognize an eligible capital gain but have a 180-day Opportunity Zone investment window that closes before enhanced OZ incentives become effective in 2027. One strategy, the “Bridge Strategy,” is to invest the gain in a Qualified Opportunity Fund to obtain temporary deferral and then dispose of the QOF interest before the statutory recognition date of December 31, 2026. Under the final regulations, the resulting gain recognition starts a new 180-day reinvestment period, potentially allowing the taxpayer to make a qualifying investment after the enhanced incentives take effect.

How a current OZ investor could position themselves to gain OZ 2.0 incentives.

- A taxpayer deferred a 2022 capital gain by investing in a QOF. In November 2026, they sold the original QOF, opening a new 180-day reinvestment window. Because the QOF was sold before a ten-year hold was achieved, the recognized gain would consist of the originally deferred gain, adjusted for any appreciation or loss in the QOF’s value. They could then reinvest the resulting gain into a new QOF in early 2027 to re-defer their tax liability. That new investment would be eligible for the enhanced OZ 2.0 benefits and have a new holding period

How an existing QOF investor can achieve the elimination benefit sooner.

- The taxpayer may decide to stay invested in the original QOF. By not exiting the QOF, they keep their original holding period. This enables them to eliminate 100% of any QOF capital gains sooner, which would be 10 years from the date of the QOF investment. Under OZ 1.0 rules, the elimination benefit would remain available through 2047. The deferral period would end on December 31, 2026, and the tax on the original capital gain would be due in the spring of 2027.

- The 10-year clock for complete elimination of any capital gain on the QOF resets to zero each time they reinvest in a new QOF, so investors bridging from one QOF to another will need to stay invested in Opportunity Zones for a timeline longer than the standard 10 years.

- Communities designated as Opportunity Zones under the new OZ regulations will have stricter eligibility standards, which could increase the riskiness of the investment.

- Making a short-term QOF investment exposes investors to the risks of price volatility.

- The re-deferral mechanism rests on the final OZ regulations themselves, rather than solely on our interpretation. That said, OZ 2.0 is newly enacted, and no IRS guidance or case law has yet addressed its interaction with the re-deferral rules. We are keeping watch for any additional guidance from the IRS on this topic.

Here are comments on the final opportunity zone regulations by the law firm of Lowenstein Sandler:

Can a taxpayer reinvest returns from a QOF into another QOF?

Yes. The Proposed Regulations provided that if a taxpayer disposed of the entire QOF interest investment with respect to a Deferred Gain, the taxpayer could make another QOF investment and effectively “re-defer” the Deferred Gain. In a taxpayer-friendly revision of the Proposed Regulations, the Final Regulations provide that even if a taxpayer disposes of less than its entire investment in a QOF, the resulting gain can be eligible for re-deferral. The 180-day reinvestment period begins on the date the QOF investment is disposed of (rather than the date of the original sale or exchange that gave rise to the eligible gain to which the inclusion event relates). Notably, the taxpayer’s holding period in the new QOF investment for purposes of the 10-year tax elimination benefits… begins on the date of the reinvestment into the new QOF. [3]

Conclusion

The “Dead Zone” problem is real, but it doesn’t have to be a roadblock for OZ investors and communities. We believe the regulatory framework already provides a pathway for investors to bridge the gap between today’s Opportunity Zone incentives and the enhanced benefits that will become available in 2027. While this strategy comes with inherent risks, it could help maintain capital flows to Opportunity Zone communities, provide investors and tax planners with additional planning flexibility, and preserve the eligibility of capital to access the enhanced Opportunity Zone 2.0 incentives when they take effect in 2027. Investors considering this approach should consult with qualified tax advisors and seek out QOFs that offer the flexibility needed to execute this strategy effectively.

Bridge your gains today to capture tomorrow’s Opportunity Zone advantages. Read our Fund Overview to see how Park View OZ makes the transition seamless.

About the Author

Michael Kelley

His publications appear regularly in Thomson Reuters journals, including Practical Tax Strategies, Real Estate Taxation, and Estate Planning, as well as The CPA Journal, Thomson Reuters’ Checkpoint and Westlaw databases, and Kiplinger’s Tax Planning and Adviser Intel columns. He has also trained over 10,000 CPAs and enrolled agents through continuing education courses focused on Opportunity Zone tax planning strategies.

Read more about the author in his biography.

Park View OZ: The Streamlined Approach to QOF Investing

Unique Public Access: Park View OZ is the only Qualified Opportunity Fund with publicly traded shares (trading symbol: PVOZ).

Flexible Entry Options: Begin with as little as one share on the open market or $10,000 through our subscription agreement.

Investment Timeline Freedom: Exit at your discretion without penalty. With no planned 10-year liquidation, maximize potential tax-free growth for 30 years.

Simplified Tax Reporting: Avoid the complexity and delays of partnership K-1 tax forms.

Open to All Investors: No accreditation requirements to participate.

Convenient Purchasing Methods: Buy shares through your existing brokerage account or directly via our website’s electronic subscription agreement.

Are you ready to see how QOFs can benefit you?

Materials provided by Park View OZ or our affiliates have been prepared for informational purposes only and are not intended to provide or be relied on for tax, legal, or financial advice. You should consult your own tax and legal advisors before engaging in any transaction.